Punkinhead

Pre-takeoff checklist

- Joined

- Sep 23, 2018

- Messages

- 107

- Display Name

Display name:

Punkinhead

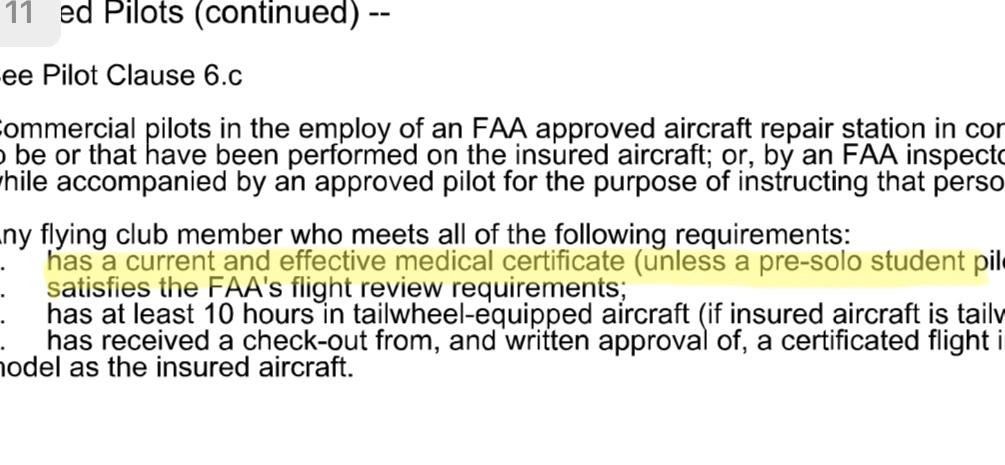

I got a quote to renew my insurance that gave me a choice of two carriers. I could stay with my current insurer (AIG) or go with a new carrier. They were within $20 of each other and the coverage was similar. I've never had a claim so I haven't had any interactions that would lead me to pick one over the other. I asked the agent if their office knew of any reason why I'd pick one over the other and she said, "well, if you ever decide to go Basicmed the new carrier won't cover you". That's kind of a big deal! I've been using Basicmed since the program started and it's written on my renewal form where I updated my hours, ratings, biennial, etc. The Class 3 medical requirement wasn't mentioned anywhere in the quote. She said AIG would cover me if I went Basicmed or sport pilot. Be careful out there...

")